#7 The State of Money Today: Stablecoins

Assessing Stability and Trust in the Pursuit of Hayek's "Good Money"

Brain farting time:

It's been almost three weeks since I published my last article about memecoins. Time really flies! Though I've written two pieces about movies I watched recently—Midway and Heretic—I feel anxious about starting research on a new topic. I read somewhere that if you're not doing something, it simply means it's more challenging than you initially thought. Well, sometimes we just need to give ourselves a gentle nudge forward.

Whether good or not, I always learn something through my research and writing. The value you find in it isn't for me to decide—though I hope you do find some. After all, it takes two to think.

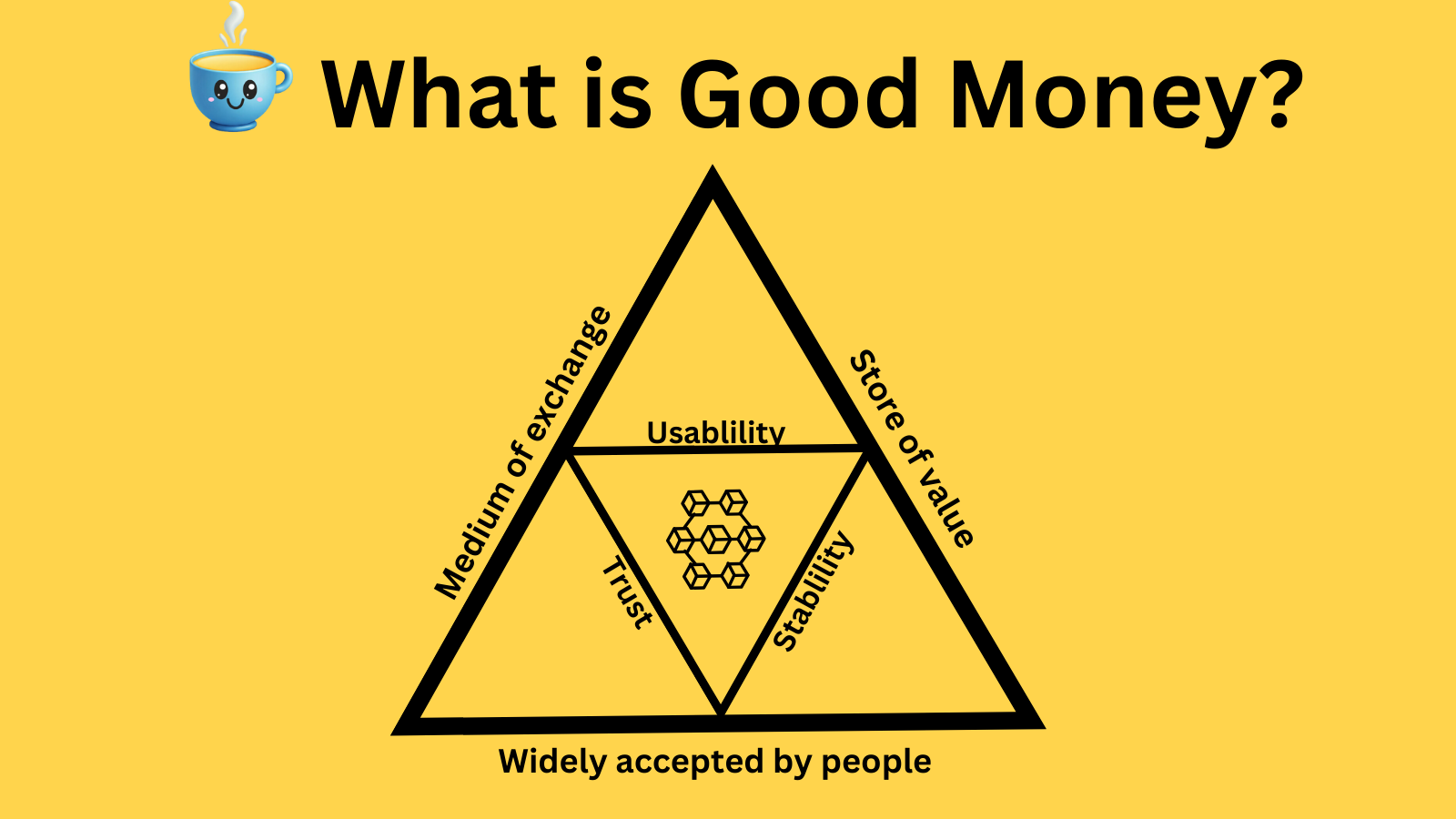

Now, let's turn to today's topic: stablecoins. This is the second-to-last topic in our series on the Denationalization of Money (with Real World Asset tokenization being the final piece). We'll evaluate the current money market using Hayek's framework of what makes "Good Money."

Before diving in, let's look at Hayek's definition of "Good Money":

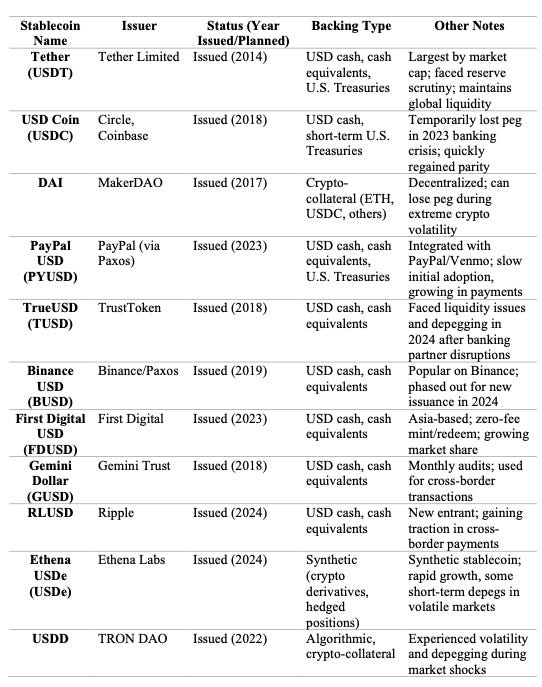

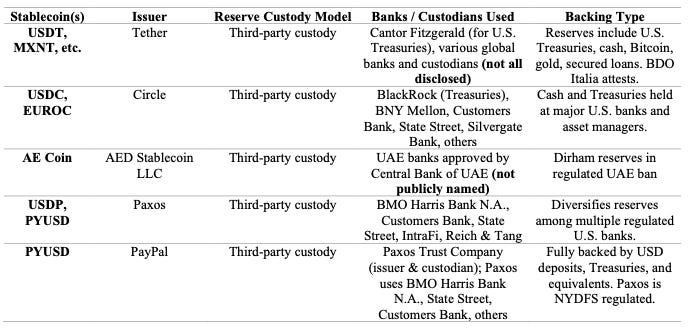

Current Stable Coin Market

Well, let’s just take a look at the list below:

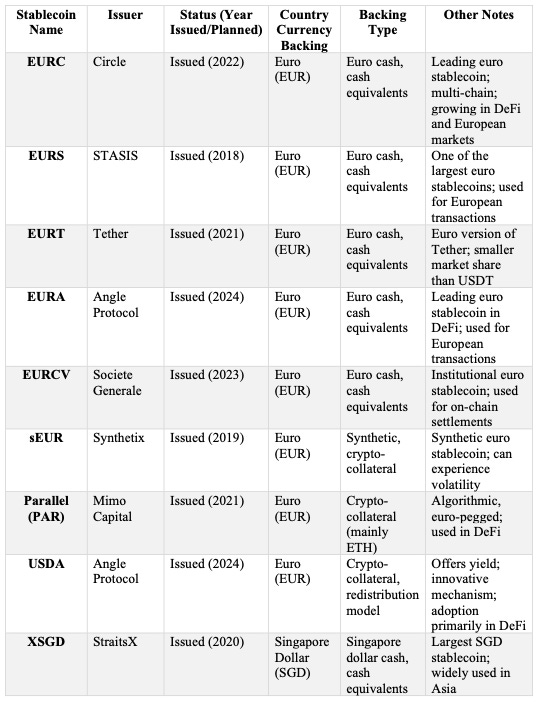

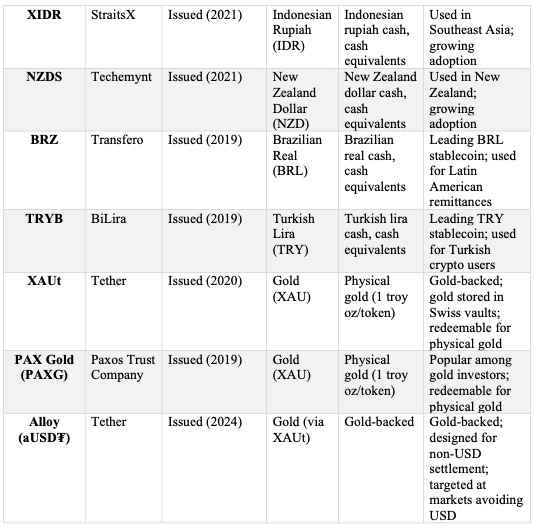

USD-Backed Stablecoins

Non-USD-backed Stablecoins:

With so many stable coins flooded the money market, we can’t help but ask: why Stable Coins?

According to Perplexity, originally, stable coins were created to

Reduce Volatility: a digital asset, unlike Bitcoin or Ethereum, that maintains a stable value

Bridge Traditional and Crypto Finance: allowing users to move value in and out of crypto markets without exposure to wild price swings

Facilitate DeFi and Trading: providing liquidity, enabling lending/borrowing, and serving as a safe haven during market downturns

Enable Everyday Use: used for daily transactions, payments, and remittances, where price stability is crucial for both merchants and consumers

And now, the impact of stable coins have evolved far beyond these original goals. Some outstanding examples:

SpaceX has been using USDT as payment for the underbanked Starlink customers since 2022.

PayPal used PYUSD to pay two major vendors: consulting firm Ernst & Young and Google for cloud services in September 2024,

Stripe began supporting USDC payouts in 2023.

Visa piloted USDC (USD Coin) settlement with Crypto.com in 2020 and expanded the program to select merchants.

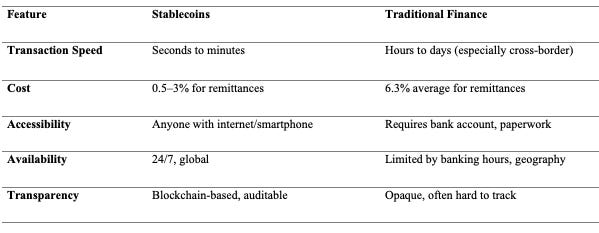

Clearly, compared to traditional finance, Stablecoins’ advantages can not be overlooked.

As good as Stablecoins seem to be, by Hayek’s stand of Good money, does stable coin belong to one of them?

Current Stable Coin’s Usage: YES, absolutely!

Current Stable Coin’s Stability and Trust:

Yes, but with a question mark.

As can be seen from the charts above, stablecoins are in general issued by private sectors. According to the EU’s MiCA and U.S. legislation (e.g., Lummis-Gillibrand Act), third-party custody is required for non-bank issuers. (Banks may self-custody reserves if they meet stringent capital and reporting standards.)

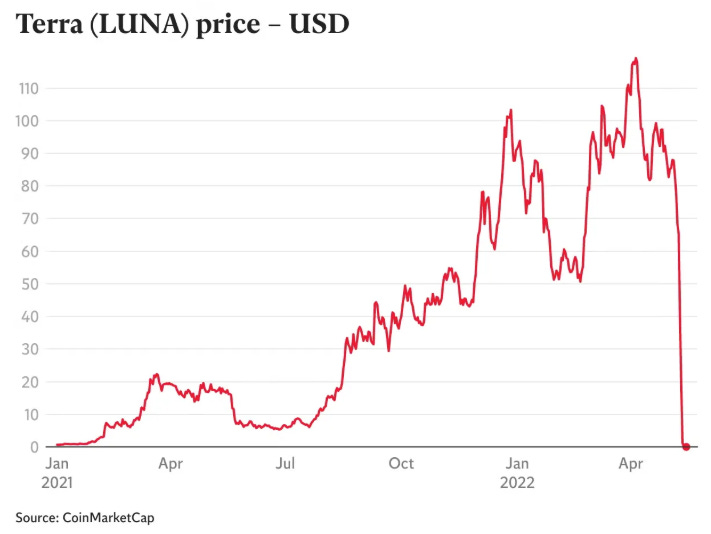

While third-party custody appears to provide safety, the TerraLuna crash remains a sobering reminder of what can go wrong.

What Happened to the Terra Luna Crash?

Again, Dr. Perplexity summarizes the crash of TerraLuna:

TerraUSD (UST) was an algorithmic stablecoin designed to keep a $1 value using a mint-and-burn mechanism with its sister token LUNA, and was backed mainly by LUNA and reserves of Bitcoin and other cryptocurrencies—not by cash or real-world assets.

When confidence faltered in May 2022, mass withdrawals triggered a "death spiral": UST lost its peg, LUNA’s supply hyperinflated, and both tokens collapsed, erasing over $40 billion in value and causing wider crypto market losses over $400 billion.

After the crash, Terra’s original blockchain and tokens were abandoned, a new Terra 2.0 chain was launched, and the event led to skepticism about algorithmic stablecoins like UST; similar projects (e.g., Ampleforth, Frax, Empty Set Dollar) have faced increased scrutiny due to these risks.

In short, Terra Luna failed because:

it had no actual pegging to USD,

it was algorithm-based, meaning prices could change at any time based on the algorithm, and

the reserves were self-managed without transparency or regulation.

While third-party custody appears secure, we must question: Are these third parties truly independent? How can we verify their independence and monitor their actions? That's one concern.

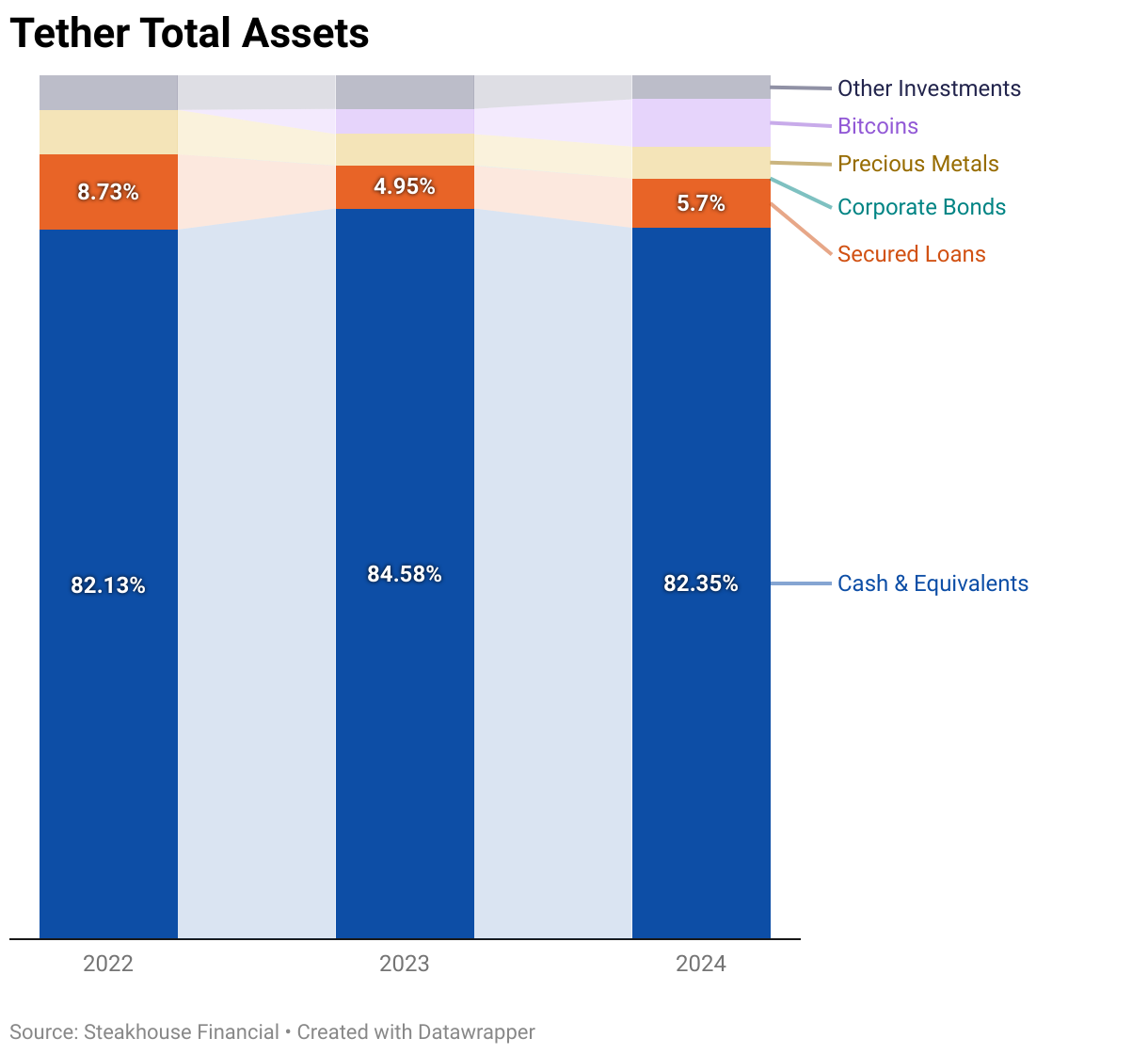

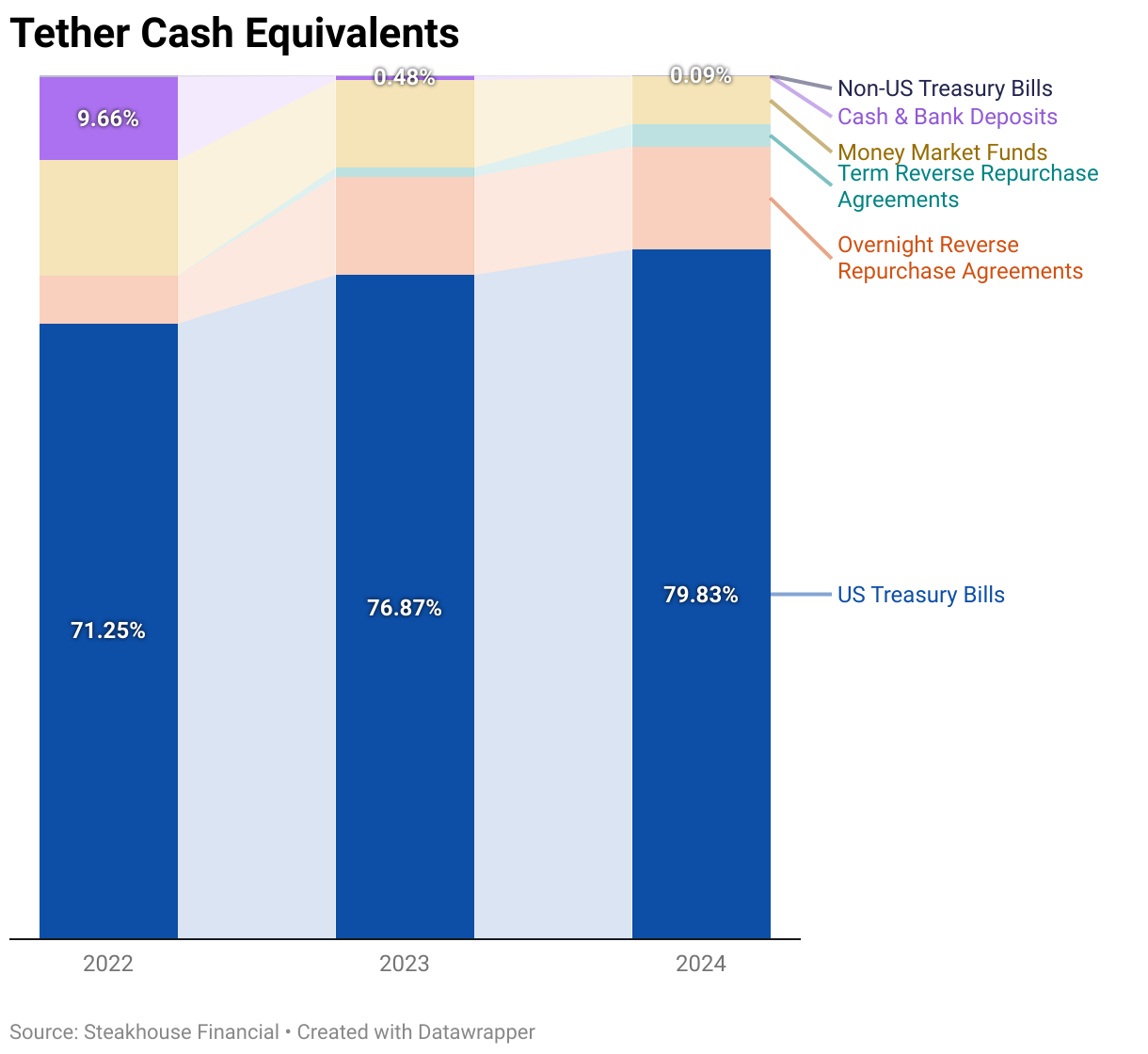

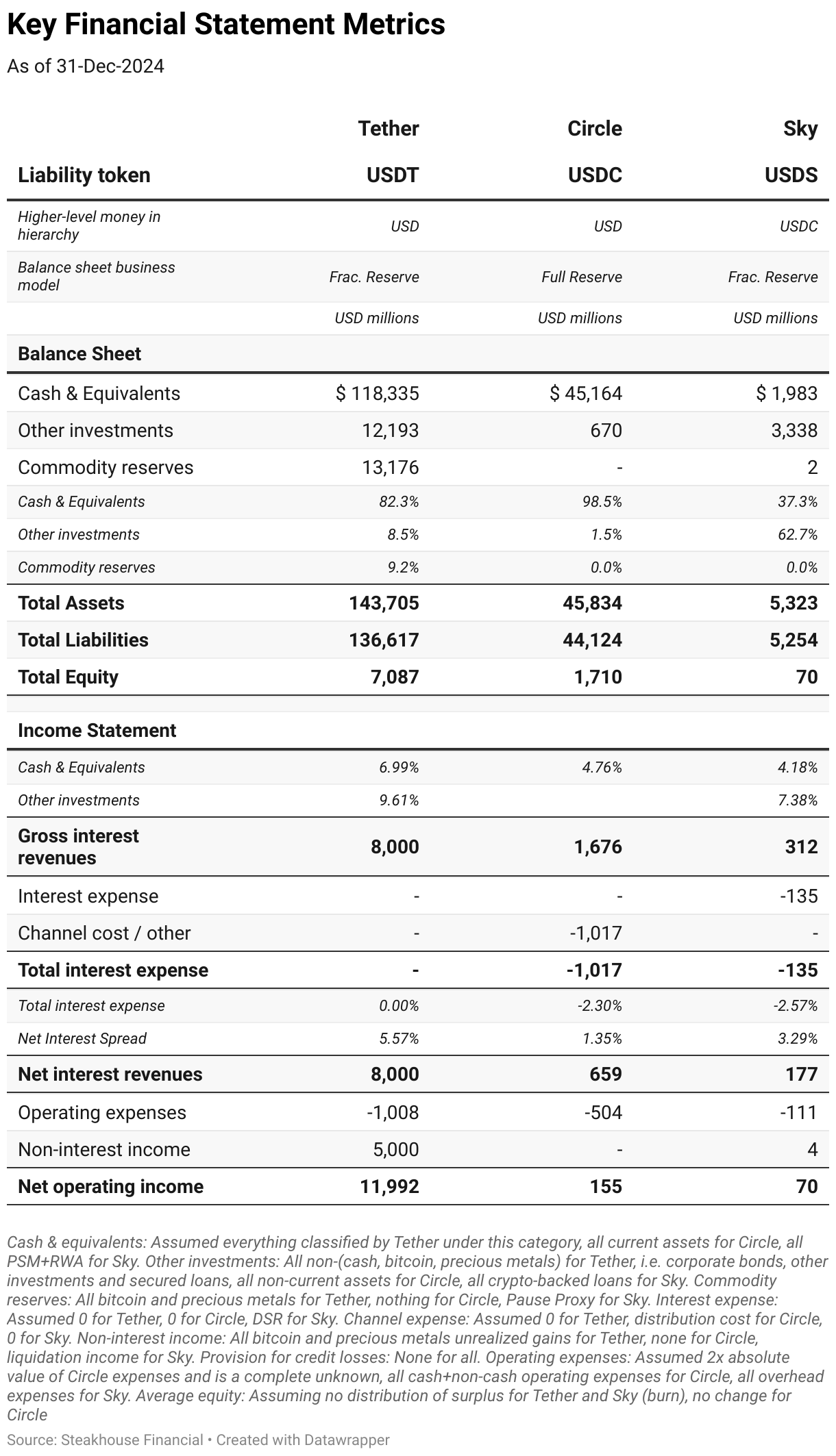

Another issue lies with "cash equivalents." These are not the same as cash—even Treasury bonds, considered safe-haven assets, can fluctuate in value. This becomes even riskier with stocks and cryptocurrencies like Bitcoin and Ethereum. The problem is that mainstream stablecoins' backing consists mainly of these "cash equivalents." In fact, no current stablecoin maintains a pure one-to-one USD peg. See below.

USDT, USDC & USDS Key Financial Statement Metrics

I think the data above speaks volumes. If we hold ourselves to Hayek's standard of Good Money—stable, usable, and trustworthy—current stablecoins fall short. Despite their usefulness, stablecoins struggle to meet the criteria of stability and usability.

Stable means the price doesn't change. As their name suggests, if a stablecoin is pegged to one dollar, it should remain one dollar at all times, period.

Third-party custody auditing and monitoring in the current money market lacks sufficient transparency and independence.

So What Makes a Stablecoin Good?

As stated above, the biggest issues for current stablecoins are twofold:

Stability—maintaining the peg at all times. The solution requires that any fiat used to mint the stablecoin must have its backing reserve remain completely untouched. This means the reserve cannot be used to fund other projects, investments, or cryptocurrency purchases. The fiat used to mint stablecoins must remain stable and immovable at all times—no algorithmic mechanisms involved.

Trust—truly independent third-party custody of reserves. This independence must be established from both technical and legal perspectives, with constant monitoring and auditing. The infrastructure should be technically immutable, implemented through transparent smart contracts that prevent anyone from making unauthorized changes, even if they wanted to.

Gold-backed stablecoins are telling a different story.

As a rare metal, gold's price has surged over 26% since the start of 2025 (the current gold futures price is around $3340 per ounce). What's interesting about stablecoins pegged to gold is that their value would naturally increase with gold prices

(for example, if 1 gold coin equals 1 gram of gold, its value against fiat currencies would rise due to gold's scarcity).

We're likely to see more gold-backed stablecoins emerge.

As more participants enter the stablecoin space, particularly with gold-backed tokens, the role of fiat currency becomes questionable. With everything moving on-chain and real-world assets being tokenized, what place will traditional finance hold? As the name suggests, it might become merely a tradition.

And that transformation may arrive sooner than we think.

Earlier articles in the series Denationalized Currency in the Age of Blockchain and AI

#1 You Don't Need to Be a Government to Create Money

#3 The State of Money Today (1) Fiat — Is Fiat Good Money?

#4 The State of Money Today (2) Bitcoin